When you get a credit card offer in the mail, or email, it may come with exciting buzzwords and marketing lingo about low fees, big rewards, and other benefits. But what will the card really cost? Thanks to the Federal government, credit card issuers have to follow a clear template that explains the costs of a card in one place. Today, we are going to dig into that template so you know what to look out for and if a credit card might make sense for you.

What is a credit card offer?

A credit card offer is a public or personalized solicitation outlining the details of a specific credit card. Offers may be on a public website, like a bank or card issuer’s website, an email to you, or a direct mailing. It doesn’t matter where you come across it, all credit card offers have to adhere to a set of rules.

It is also important to recognize what a credit card offer is not. A credit card offer does not guarantee the issuer will approve you for the new card should you apply. It simply states that you may apply, and if you do and are approved these are the terms of the account.

Credit card offers are required to contain some specific information related to the costs of keeping and using the card. While the offer may not contain every detail you need to decide whether or not to apply, you should always review the offer details before signing up.

What information is contained in a credit card offer?

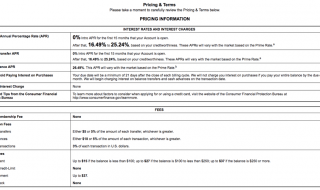

Because all credit cards are required to present the same information in the same format, we can look at any credit card to better understand what information you’ll see when you open up the offer pricing and terms. Here is a screenshot of the offer details for the Chase Freedom Unlimited credit card as of April 2018.

Here is a line-by-line breakdown of what you can find in any credit card’s pricing and terms details that come with a credit card offer. Today we are more concerned about what these terms mean than the actual values, but when you are deciding on a card you should look at every number on the terms sheet.

Interest rates and charges

Purchase Annual Percentage Rate (APR) – The APR, or annual percentage rate, is the borrowing cost for using a credit card. You can pay your card in full each month to avoid interest charges, but if you don’t pay in full and carry a balance from month to month, this is what you’ll pay to borrow those funds.

Balance Transfer APR – If you transfer a balance from another credit card, you may be charged a different interest rate. If the rate is lower, higher, or the same, it will be listed out separately from the purchase APR.

Cash Advance APR – If you want to get cash from your credit card at a bank branch or ATM, you have to pay a cash advance APR. Cash advance APRs are typically equal to or higher than the purchase APR. In the example above, the cash advance APR is equal to the highest purchase and balance transfer APR rates.

How to Avoid Paying Interest on Purchases – Banks are required to tell you how to avoid interest when using a credit card. Follow those tips to avoid those expensive interest charges if at all possible.

Minimum Interest Charge – If you do pay interest, some banks use a minimum charge for the smallest balances. In this case, the minimum is zero, but that is not the norm.

Fees

Annual Membership Fee – Some credit cards charge an annual fee to keep the account open. This is common with secured credit cards and high end rewards cards. For rewards cards, never pay more than you get back in value from a card. For secured and other cards, consider the fee on a case-by-case basis.

Transaction Fees – Balance transfers, cash advances, and foreign transactions may all incur additional fees. It is common to see fees in the 3% to 5% range for any of this type of activity. You can always avoid transaction fees by avoiding the specific activity that incurs fees. For example, if you avoid cash advances, you’ll never pay cash advance fees (or higher cash advance interest rates).

Penalty Fees – Like transaction fees, you can avoid penalty fees if you avoid penalty incurring activity. These penalty situations hurt your credit score too, so don’t ignore these! Always pay on-time, keep your credit balance below the limit, and make sure your payments won’t overdraft your checking and you should be good to go!

Terms and conditions

Every card issuer has a team of lawyers that makes sure it follows the law, and those lawyers are big on disclosures and fine print. While those dense paragraphs filled with interest rates, fees, and rules are not fun to read, it is a good idea to know what you are signing up for.

In most cases, the terms and conditions explains specific rules for residents of certain states, rules for how certain transactions are treated, and important agreements you make with the bank to open up a card. If you don’t like the agreement, don’t open the card. You most likely won’t be able to convince a bank to custom tailor their rules for you.

One of the most important lines you will find in all credit card offers: rates, fees, and terms may change in the future. Stay up-to-date with any new card rules so you don’t accidently make a costly mistake. Banks are required to notify you when terms and conditions change, so stay alert and keep your eyes on your inbox for notifications about changes, like higher interest rates and fees.

Only make informed credit decisions

Credit cards are serious business, and making good or bad credit card decisions could have a long lasting impact on your finances. Don’t go blindly into a new financial agreement. Instead, follow along with the basic credit card offer outline so you know what you’re getting into.

With the right information, you can make an informed credit card decision. There is no right or wrong for everyone, just what’s right or wrong for you. And based on the credit card offer terms, you may find the next credit card that is perfect for your wallet, or one that should send you running to the hills. It’s all in the credit card offer details. Now you know what to look for the next time a card offer shows up in your mailbox.