The fact that credit inquiries can potentially have the ability to lower credit scores is a thorn in the side of many consumers and consumer advocates. An inquiry appears on your reports to show that someone has pulled your credit history for review.

Inquiries can occur when you apply for a loan, a credit card, when you check your own credit, and even when credit card companies send you pre-approved offers in the mail.

Some of these inquiries “count” in your score, and some do not.

Why Inquiries Are Considered

Many people believe having their credit scores dinged simply for shopping around for new credit is unfair. Looking at it from a lender’s perspective, you can see how inquiries can help them to predict risk.

It’s simple math…the more credit you’re acquiring the more risky you become.

[inline-ad]Credit scoring models used by lenders, such as those built by FICO and VantageScore, are required by the Equal Credit Opportunity Act (ECOA) to be “empirically derived” and “demonstrably and statistically sound.” In other words, these scoring models cannot be developed based on guesses or assumptions.

They must be built using a scientific process and they must be proven to before lenders can legally use them. It is a fact that more inquiries equal more credit risk.

That’s why each inquiry on your credit reports will slightly affect your scores. Your score is calculated to give lenders an objective view of how risky of a borrower you are. The more credit you are trying to obtain, the more opportunities you will have to default, therefore the riskier you are to lend to.

How Much Do Inquiries Matter?

While inquiries do matter, they don’t affect your credit scores nearly as much as other factors such as payment history or credit card balances.

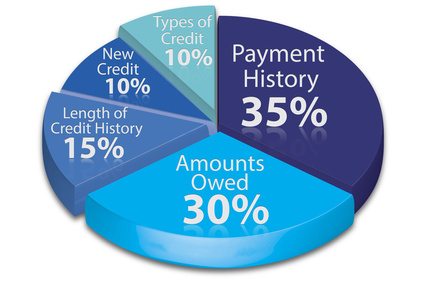

In fact, only 10% of your FICO scores are influenced by inquiries (or the lack thereof) and in the VantageScore scoring model they are considered to be among the least important factors that influence your VantageScore credit scores.

How Inquiries Are Considered

The idea that each inquiry will cost you a specific number of credit score points is a complete myth. Inquiries are not, for example, worth X number of points each. That is simply not the way that credit scoring models work. Individual items are not assigned a specific number of points.

Instead, groups of credit items are weighed as a whole. Credit scores are built from the ground up, meaning that they start at the lowest possible score (300 in FICO and newer VantageScore versions) and work their way upwards.

You do not “lose” a specific number of points when an inquiry shows up on your credit report. Rather, you could potentially earn fewer points than you would have earned before the inquiries was present.

Here is an example of how the consideration of inquiries might work. The credit scoring model will look at your credit report for the answer to a specific question such as, “What is the number of inquiries that occurred within the past 12 months?” The answer to the question would fall into one of a number of pre-defined ranges or “classes.” Those specific ranges would be worth a certain number of points.

Hypothetical Examples:

0 Inquiries = 55 Points Added to Credit Score

1 Inquiry = 50 Points Added to Credit Score

2-4 Inquiries = 40 Points Added to Credit Score

5-6 Inquiries = 25 Points Added to Credit Score

7-8 Inquiries = 10 Points Added to Credit Score

9+ Inquiries = 0 Points Added to Credit Score

The categories and the points above are purely for illustration purposes. These are not the real ranges nor are they the real points values assigned by FICO or VantageScore.

However, the premise behind the example is real. Credit scoring models consider the total number of inquiries appearing on your credit reports instead of calculating each inquiry individually.